Mettler-Toledo’s 25.7% return over the past six months has outpaced the S&P 500 by 9.4%, and its stock price has climbed to $1,406 per share. This run-up might have investors contemplating their next move.

Is now the time to buy Mettler-Toledo, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is Mettler-Toledo Not Exciting?

We’re happy investors have made money, but we're cautious about Mettler-Toledo. Here are three reasons why MTD doesn't excite us and a stock we'd rather own.

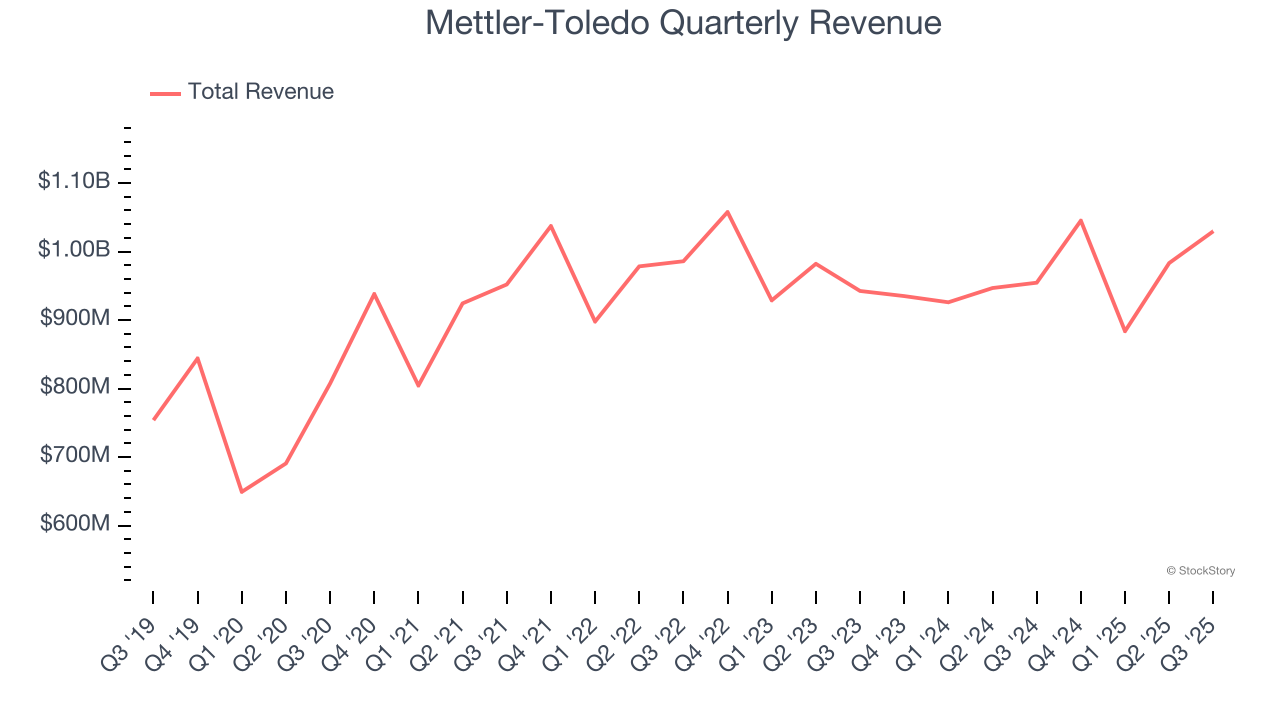

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Mettler-Toledo grew its sales at a mediocre 5.7% compounded annual growth rate. This fell short of our benchmark for the healthcare sector.

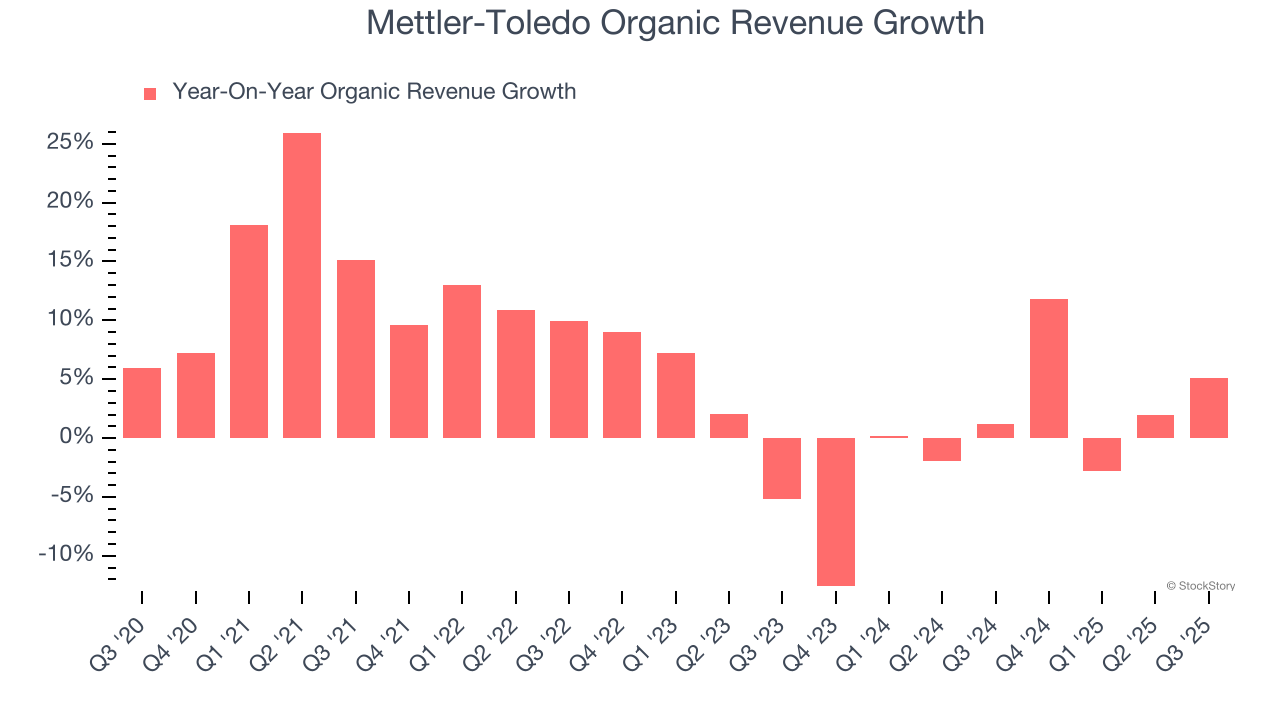

2. Core Business Falling Behind as Demand Plateaus

In addition to reported revenue, organic revenue is a useful data point for analyzing Research Tools & Consumables companies. This metric gives visibility into Mettler-Toledo’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Mettler-Toledo failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Mettler-Toledo might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

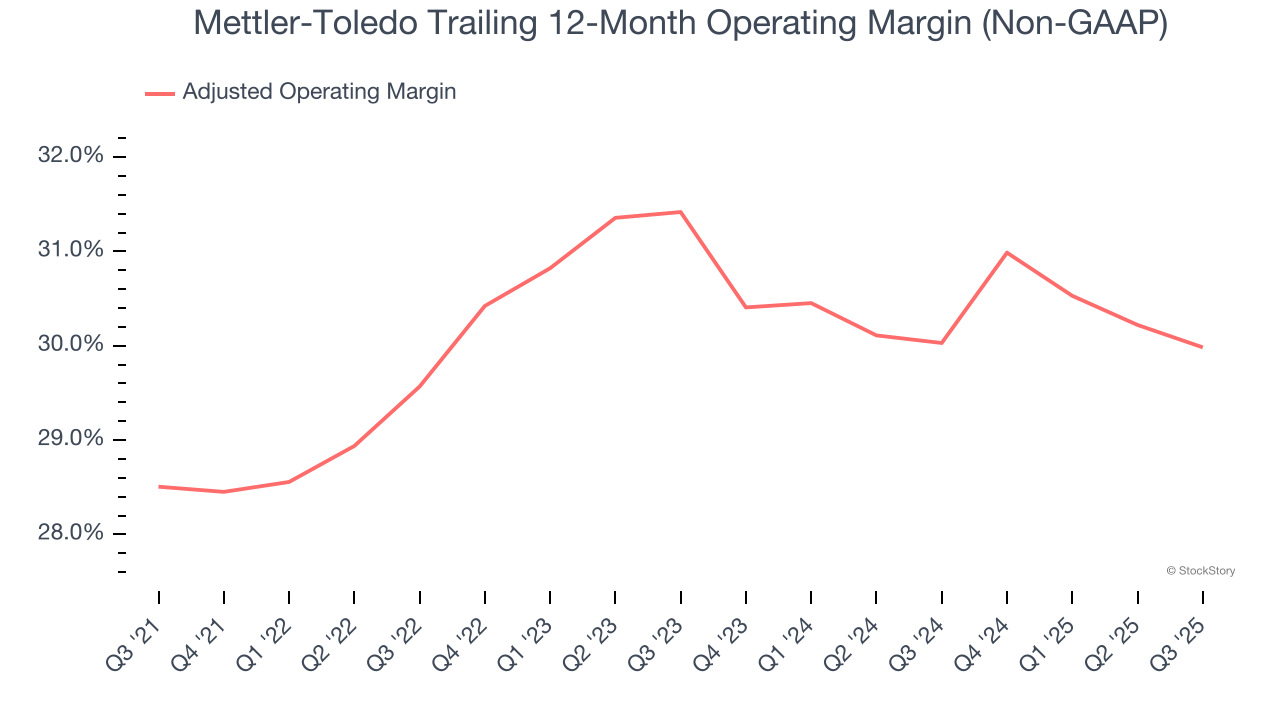

3. Shrinking Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Analyzing the trend in its profitability, Mettler-Toledo’s adjusted operating margin decreased by 1.4 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 30%.

Final Judgment

Mettler-Toledo isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 32.6× forward P/E (or $1,406 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Mettler-Toledo

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.