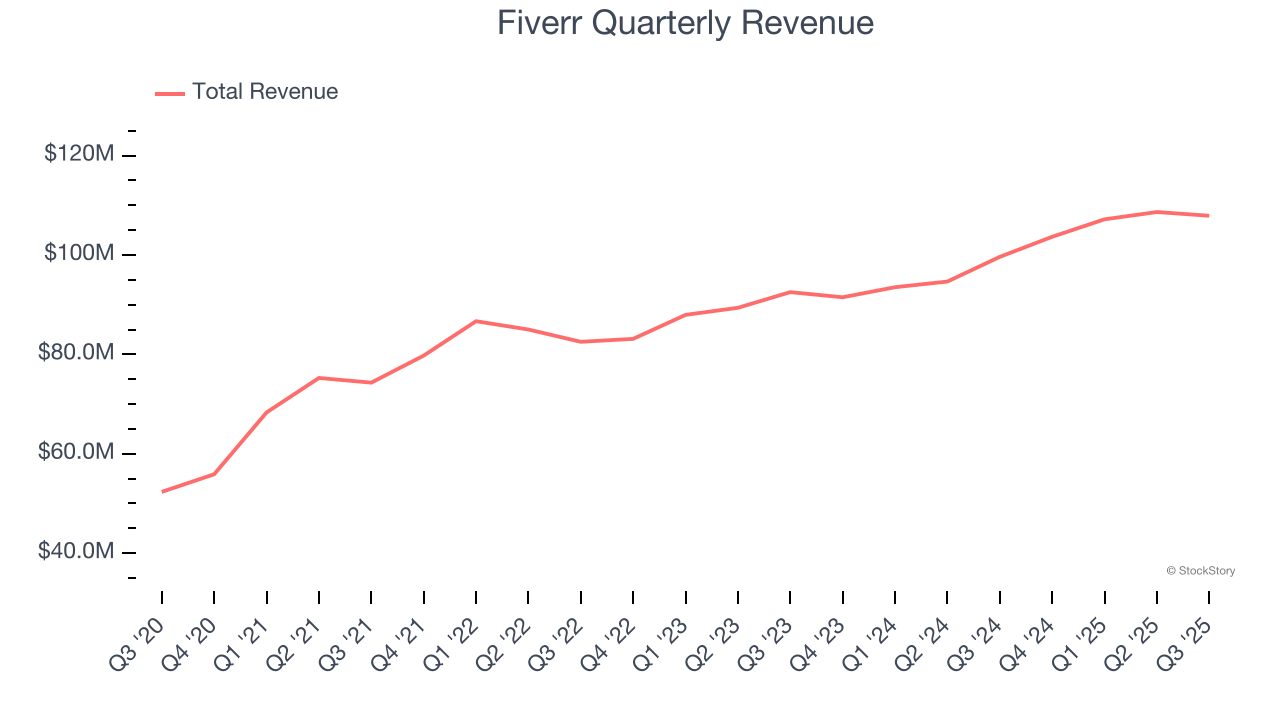

Online freelance marketplace Fiverr (NYSE:FVRR) met Wall Streets revenue expectations in Q3 CY2025, with sales up 8.3% year on year to $107.9 million. On the other hand, next quarter’s revenue guidance of $108.3 million was less impressive, coming in 0.9% below analysts’ estimates. Its non-GAAP profit of $0.84 per share was 22.9% above analysts’ consensus estimates.

Is now the time to buy Fiverr? Find out by accessing our full research report, it’s free for active Edge members.

Fiverr (FVRR) Q3 CY2025 Highlights:

- Revenue: $107.9 million vs analyst estimates of $107.9 million (8.3% year-on-year growth, in line)

- Adjusted EPS: $0.84 vs analyst estimates of $0.68 (22.9% beat)

- Adjusted EBITDA: $24.18 million vs analyst estimates of $22.37 million (22.4% margin, 8.1% beat)

- Revenue Guidance for Q4 CY2025 is $108.3 million at the midpoint, below analyst estimates of $109.3 million

- EBITDA guidance for the full year is $90.5 million at the midpoint, above analyst estimates of $87.51 million

- Operating Margin: 0.1%, up from -3.5% in the same quarter last year

- Free Cash Flow Margin: 27%, up from 23% in the previous quarter

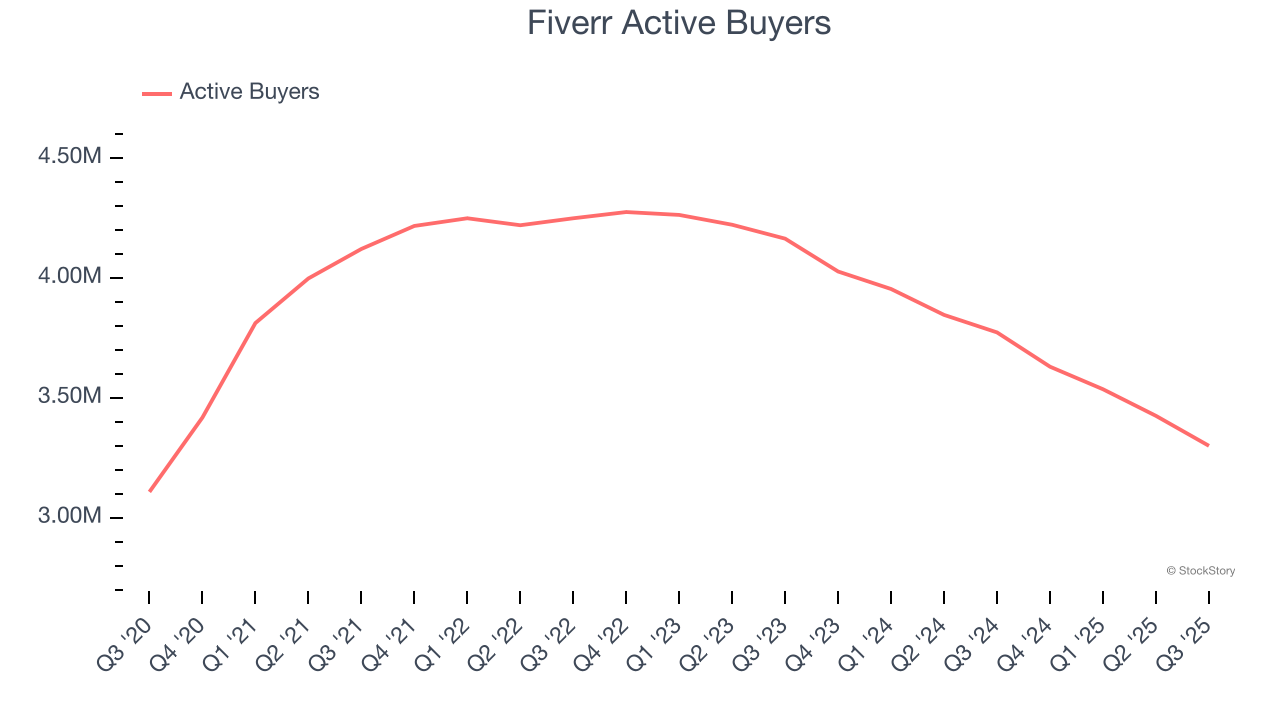

- Active Buyers: 3.3 million, down 473,000 year on year

- Market Capitalization: $798.9 million

“With AI continuing to run through every facet of the business, our commitment to driving AI transformation and re-accelerating GMV growth is as focused as ever. Our recent strategic restructuring has prepared us to further this transformation and truly establish an AI-first mentality. What the market wants is clear, high-quality specialized talent, and the intentional investments we are making are already allowing us to capture these higher-value client projects,” said Micha Kaufman, founder and CEO of Fiverr.

Company Overview

Based in Tel Aviv, Fiverr (NYSE:FVRR) operates a fixed price global freelance marketplace for digital services.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, Fiverr grew its sales at a mediocre 8.6% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Fiverr.

This quarter, Fiverr grew its revenue by 8.3% year on year, and its $107.9 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 4.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.2% over the next 12 months, a slight deceleration versus the last three years. This projection is underwhelming and implies its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Active Buyers

Buyer Growth

As a gig economy marketplace, Fiverr generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Fiverr struggled with new customer acquisition over the last two years as its active buyers have declined by 9.4% annually to 3.3 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Fiverr wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q3, Fiverr’s active buyers once again decreased by 473,000, a 12.5% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

Revenue Per Buyer

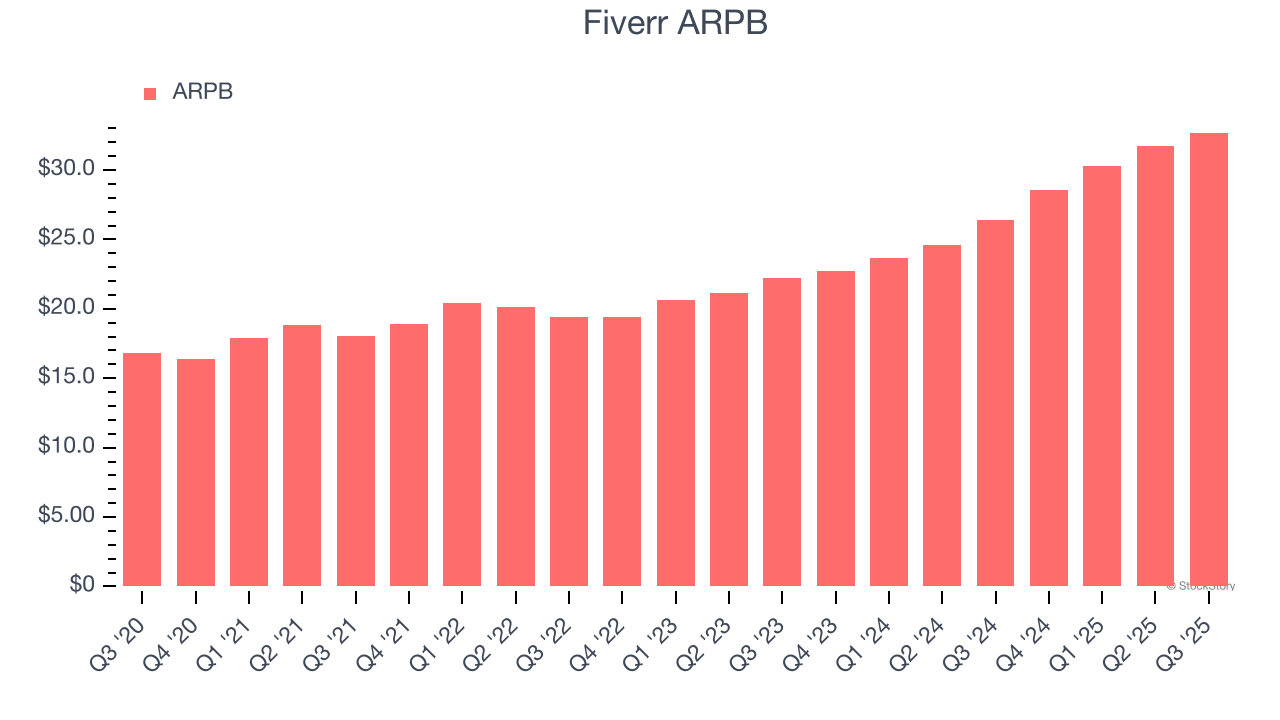

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the company earns in transaction fees from each buyer. This number also informs us about Fiverr’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Fiverr’s ARPB growth has been exceptional over the last two years, averaging 21.6%. Although its active buyers shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing buyers.

This quarter, Fiverr’s ARPB clocked in at $32.70. It grew by 23.8% year on year, faster than its active buyers.

Key Takeaways from Fiverr’s Q3 Results

We were impressed by Fiverr’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its number of buyers declined and its number of active buyers fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock traded up 5% to $22.70 immediately following the results.

So should you invest in Fiverr right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.