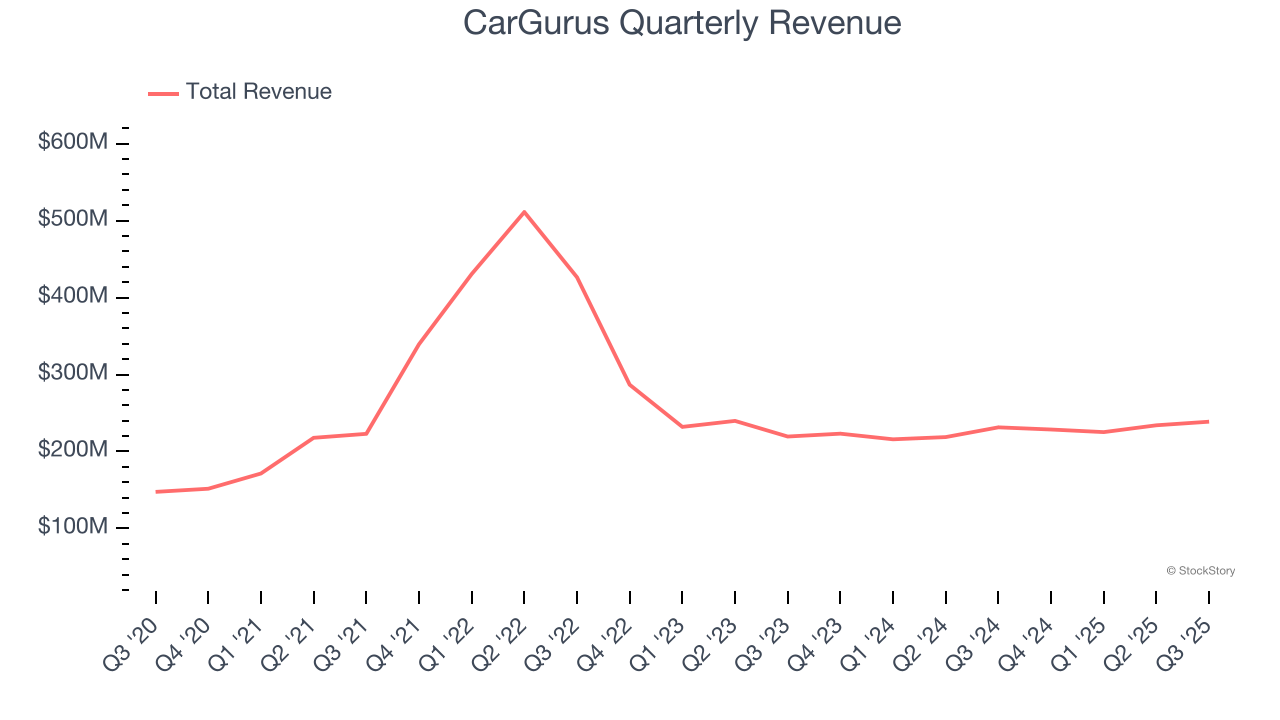

Online auto marketplace CarGurus (NASDAQ:CARG) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 3.2% year on year to $238.7 million. Guidance for next quarter’s revenue was better than expected at $238.5 million at the midpoint, 0.6% above analysts’ estimates. Its non-GAAP profit of $0.57 per share was 3.7% above analysts’ consensus estimates.

Is now the time to buy CarGurus? Find out by accessing our full research report, it’s free for active Edge members.

CarGurus (CARG) Q3 CY2025 Highlights:

- Revenue: $238.7 million vs analyst estimates of $235 million (3.2% year-on-year growth, 1.6% beat)

- Adjusted EPS: $0.57 vs analyst estimates of $0.55 (3.7% beat)

- Adjusted EBITDA: $78.67 billion vs analyst estimates of $76.39 million (32,957% margin, significant beat)

- Revenue Guidance for Q4 CY2025 is $238.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q4 CY2025 is $0.64 at the midpoint, above analyst estimates of $0.61

- EBITDA guidance for Q4 CY2025 is $87 million at the midpoint, above analyst estimates of $84.27 million

- Operating Margin: 22.9%, up from 11.9% in the same quarter last year

- Free Cash Flow Margin: 26.8%, down from 27.9% in the previous quarter

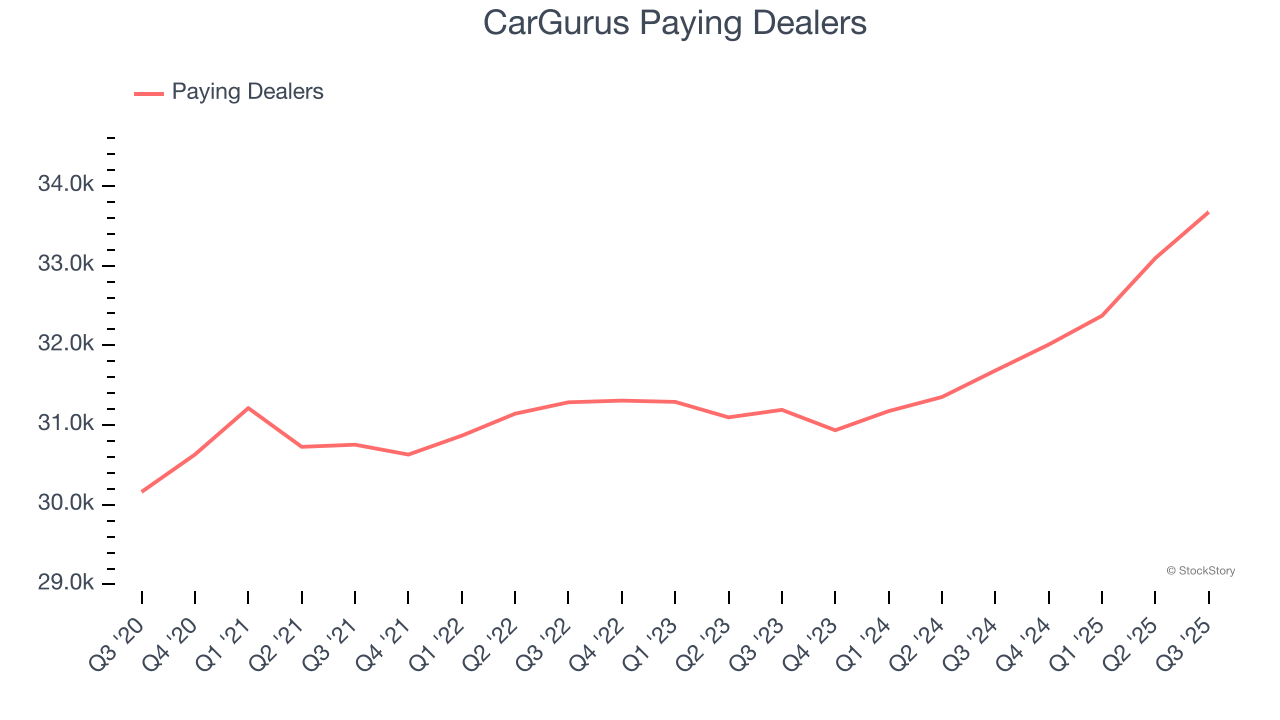

- Paying Dealers: 33,673, up 1,989 year on year

- Market Capitalization: $3.38 billion

“We delivered another quarter of strong Marketplace revenue growth as dealers have increasingly adopted our data-driven tools,” said Jason Trevisan, Chief Executive Officer at CarGurus.

Company Overview

Bringing transparency to a sometimes opaque process, CarGurus (NASDAQ:CARG) is a digital marketplace where auto dealers can connect with potential customers and where car buyers can browse, purchase, and obtain financing.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. CarGurus struggled to consistently generate demand over the last three years as its sales dropped at a 18.4% annual rate. This wasn’t a great result and is a tough starting point for our analysis.

This quarter, CarGurus reported modest year-on-year revenue growth of 3.2% but beat Wall Street’s estimates by 1.6%. Company management is currently guiding for a 4.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Paying Dealers

User Growth

As an online marketplace, CarGurus generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, CarGurus’s paying dealers, a key performance metric for the company, increased by 2.5% annually to 33,673 in the latest quarter. This growth rate is one of the lowest in the consumer internet sector. If CarGurus wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

In Q3, CarGurus added 1,989 paying dealers, leading to 6.3% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

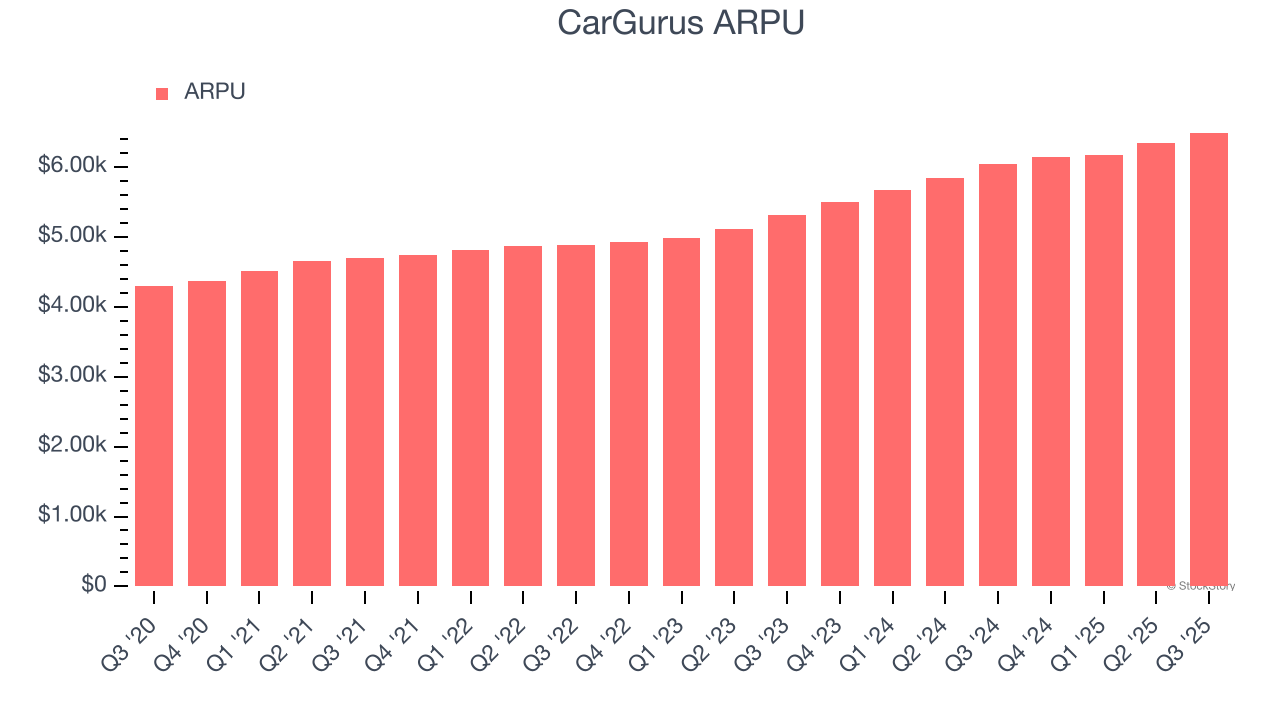

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and CarGurus’s take rate, or "cut", on each order.

CarGurus’s ARPU growth has been exceptional over the last two years, averaging 11.3%. Its ability to increase monetization while growing its paying dealers demonstrates its platform’s value, as its users are spending significantly more than last year.

This quarter, CarGurus’s ARPU clocked in at $6,492. It grew by 7.5% year on year, faster than its paying dealers.

Key Takeaways from CarGurus’s Q3 Results

We were impressed by how significantly CarGurus blew past analysts’ EBITDA expectations this quarter. We were also glad its EBITDA guidance for next quarter exceeded Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 5.6% to $35 immediately after reporting.

Sure, CarGurus had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.