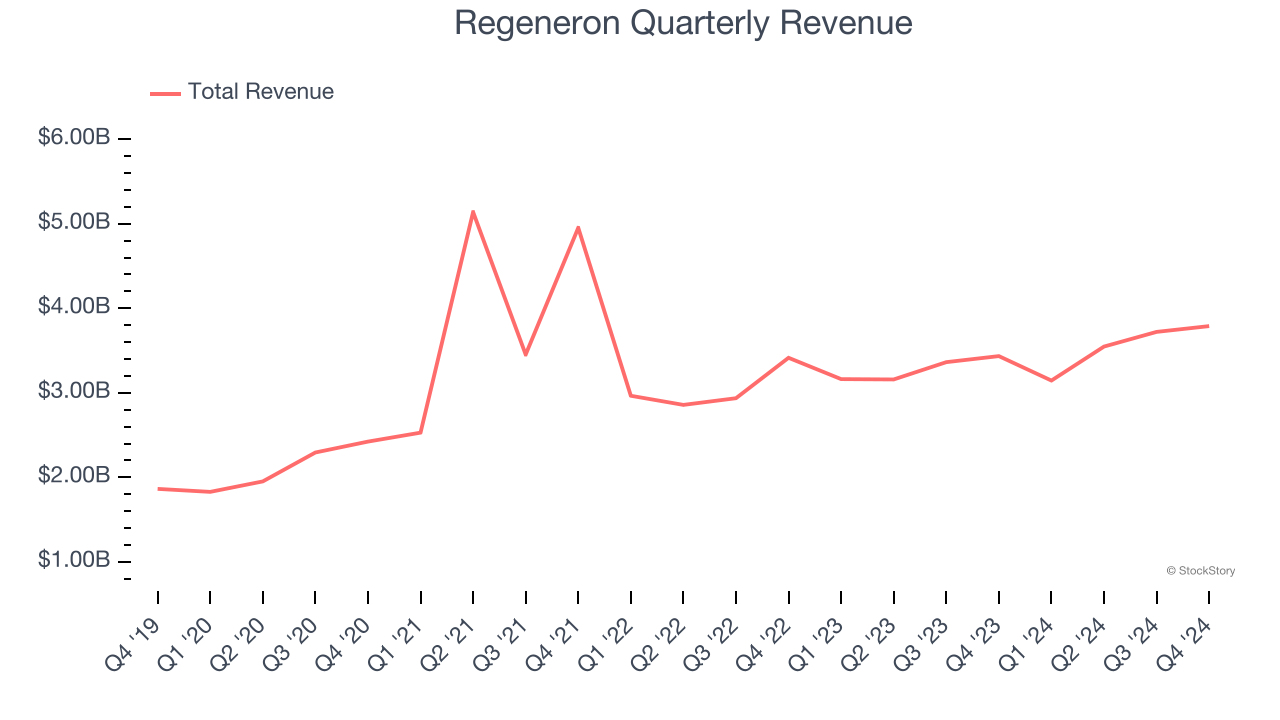

Biotech company Regeneron (NASDAQ:REGN) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 10.3% year on year to $3.79 billion. Its non-GAAP profit of $12.07 per share was 7.8% above analysts’ consensus estimates.

Is now the time to buy Regeneron? Find out by accessing our full research report, it’s free.

Regeneron (REGN) Q4 CY2024 Highlights:

- Initiated an $0.88 quarterly dividend

- Revenue: $3.79 billion vs analyst estimates of $3.75 billion (10.3% year-on-year growth, 1% beat)

- Adjusted EPS: $12.07 vs analyst estimates of $11.19 (7.8% beat)

- Operating Margin: 26.1%, down from 28.3% in the same quarter last year

- Market Capitalization: $71.75 billion

"Regeneron's financial and commercial strength allows for continued investment in our industry-leading R&D pipeline, while simultaneously returning capital to our shareholders through our newly initiated dividend program and increased share repurchase capacity," said Leonard S. Schleifer, M.D., Ph.D., Board co-Chair, President and Chief Executive Officer of Regeneron.

Company Overview

Founded in 1988 as a small research firm, Regeneron (NASDAQ:REGN) is a biopharmaceutical company that develops and manufactures innovative medicines, with a focus on eye diseases, cancer, and rare genetic disorders.

Immuno-Oncology

Over the next few years, immuno-oncology companies, which harness the immune system to fight illnesses such as cancer, faces strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Sales Growth

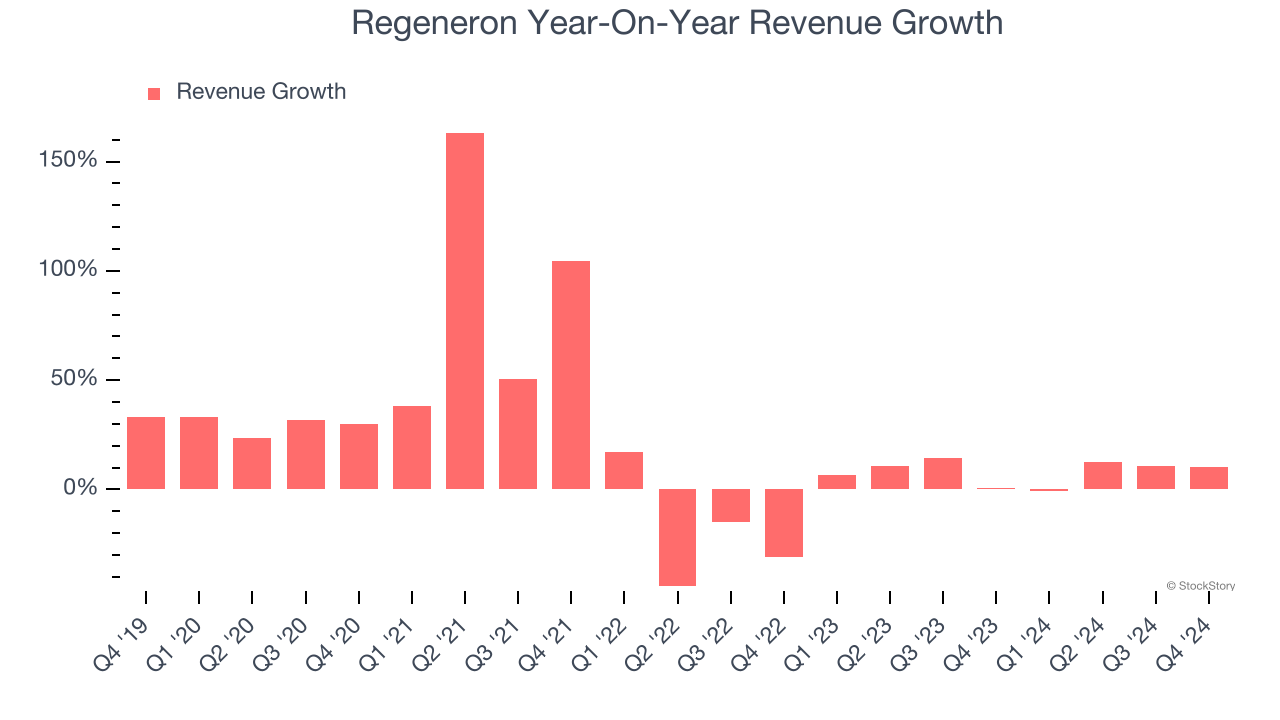

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Regeneron’s 16.7% annualized revenue growth over the last five years was impressive. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Regeneron’s annualized revenue growth of 8% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Collaboration and Product & Pipeline, which are 42.4% and 52.9% of revenue. Over the last two years, Regeneron’s Collaboration revenue averaged 12.7% year-on-year growth while its Product & Pipeline revenue averaged 5.2% growth.

This quarter, Regeneron reported year-on-year revenue growth of 10.3%, and its $3.79 billion of revenue exceeded Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

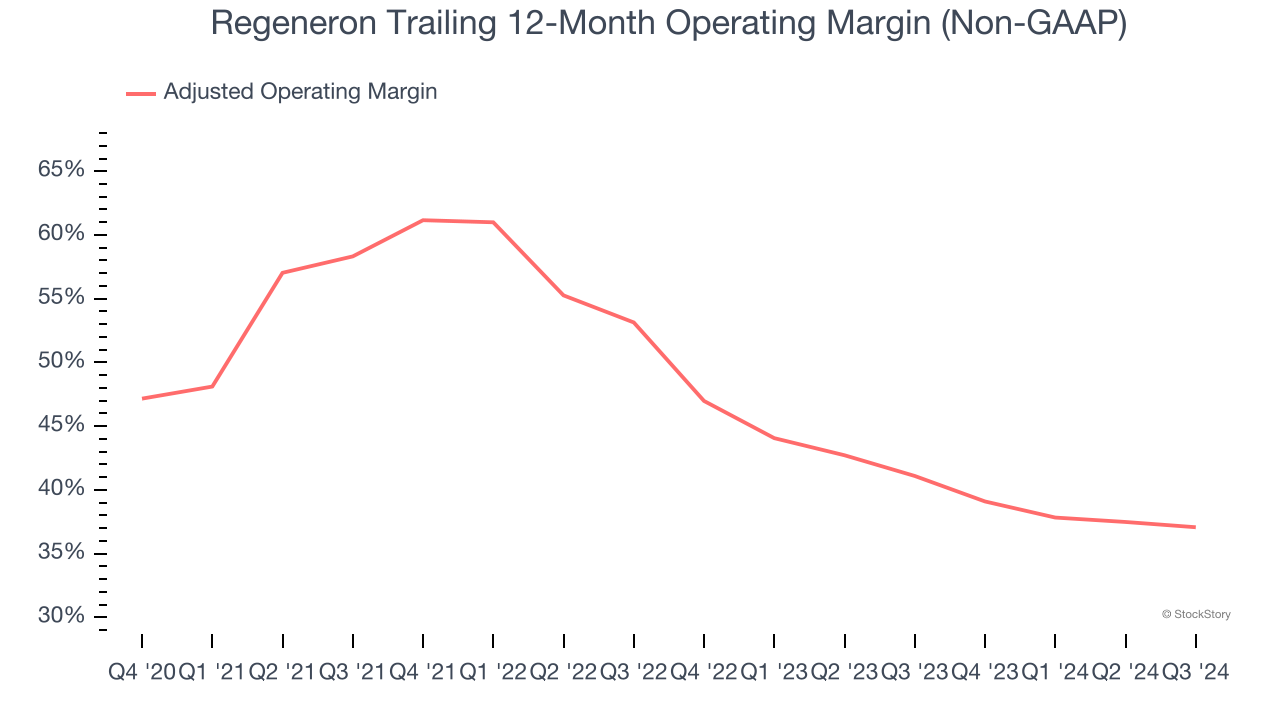

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Regeneron has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 47.3%.

Looking at the trend in its profitability, Regeneron’s adjusted operating margin decreased by 9.7 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 10.8 percentage points on a two-year basis. We’re disappointed in these results because it shows operating expenses were rising and it couldn’t pass those costs onto its customers.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

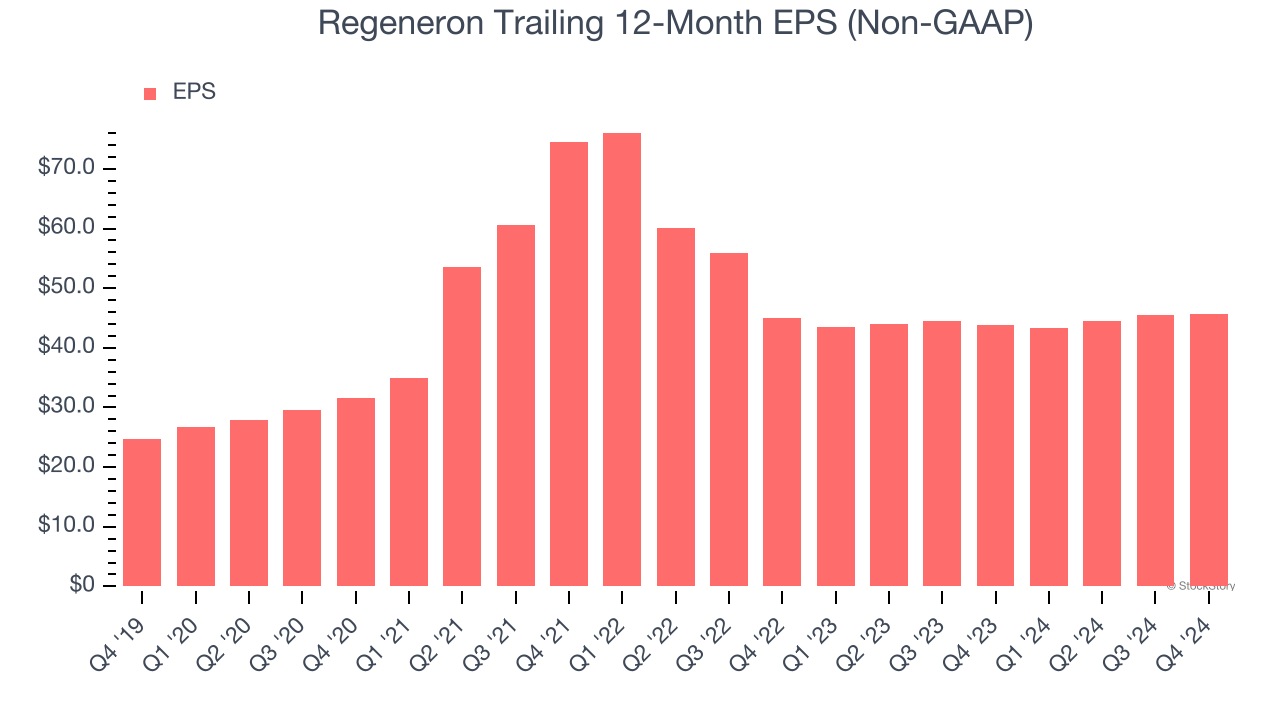

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Regeneron’s EPS grew at a spectacular 13.1% compounded annual growth rate over the last five years. However, this performance was lower than its 16.7% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Regeneron’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Regeneron’s adjusted operating margin declined by 9.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Regeneron reported EPS at $12.07, up from $11.86 in the same quarter last year. This print beat analysts’ estimates by 7.8%. Over the next 12 months, Wall Street expects Regeneron’s full-year EPS of $45.64 to stay about the same.

Key Takeaways from Regeneron’s Q4 Results

It was good to see Regeneron narrowly top analysts’ revenue expectations this quarter. We were also glad it blew past Wall Street's EPS estimates and initiated a dividend of $0.88 per share. Overall, this quarter had some key positives. The stock traded up 5.8% to $705 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.