Engineering and automation solutions company Emerson (NYSE:EMR) fell short of the market’s revenue expectations in Q4 CY2024 as sales only rose 1.4% year on year to $4.18 billion. Next quarter’s revenue guidance of $4.38 billion underwhelmed, coming in 2.6% below analysts’ estimates. Its non-GAAP profit of $1.38 per share was 8% above analysts’ consensus estimates.

Is now the time to buy Emerson Electric? Find out by accessing our full research report, it’s free.

Emerson Electric (EMR) Q4 CY2024 Highlights:

- Revenue: $4.18 billion vs analyst estimates of $4.22 billion (1.4% year-on-year growth, 1.1% miss)

- Adjusted EPS: $1.38 vs analyst estimates of $1.28 (8% beat)

- Adjusted EBITDA: $1.17 billion vs analyst estimates of $1.10 billion (28% margin, 5.8% beat)

- Revenue Guidance for Q1 CY2025 is $4.38 billion at the midpoint, below analyst estimates of $4.49 billion

- Management reiterated its full-year Adjusted EPS guidance of $5.95 at the midpoint

- Operating Margin: 24.2%, up from 21.2% in the same quarter last year

- Free Cash Flow Margin: 16.6%, up from 8.2% in the same quarter last year

- Market Capitalization: $72.72 billion

"Emerson began the fiscal year on a strong note, exceeding first quarter expectations for incremental operating margins and earnings per share with strong cash flow generation," said Emerson President and Chief Executive Officer Lal Karsanbhai.

Company Overview

Founded in 1890, Emerson Electric (NYSE:EMR) is a multinational technology and engineering company providing solutions in the industrial, commercial, and residential markets.

Internet of Things

Industrial Internet of Things (IoT) companies are buoyed by the secular trend of a more connected world. They often specialize in nascent areas such as hardware and services for factory automation, fleet tracking, or smart home technologies. Those who play their cards right can generate recurring subscription revenues by providing cloud-based software services, boosting their margins. On the other hand, if the technologies these companies have invested in don’t pan out, they may have to make costly pivots.

Sales Growth

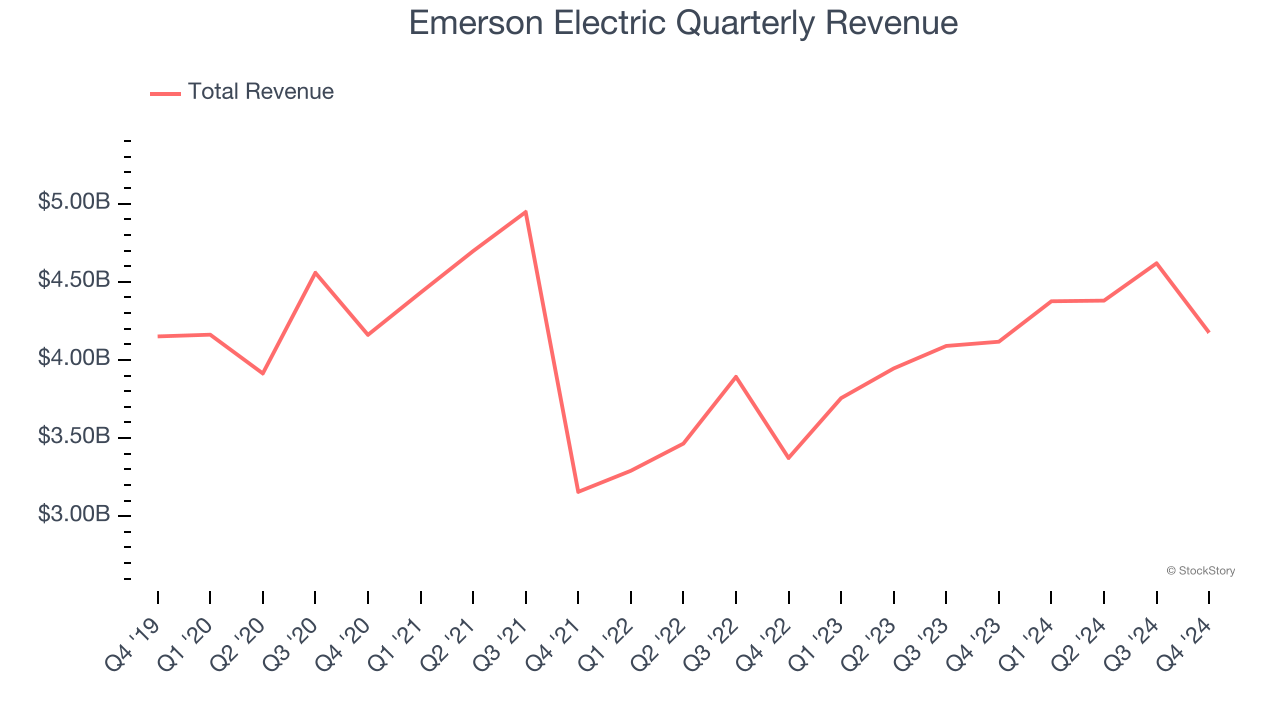

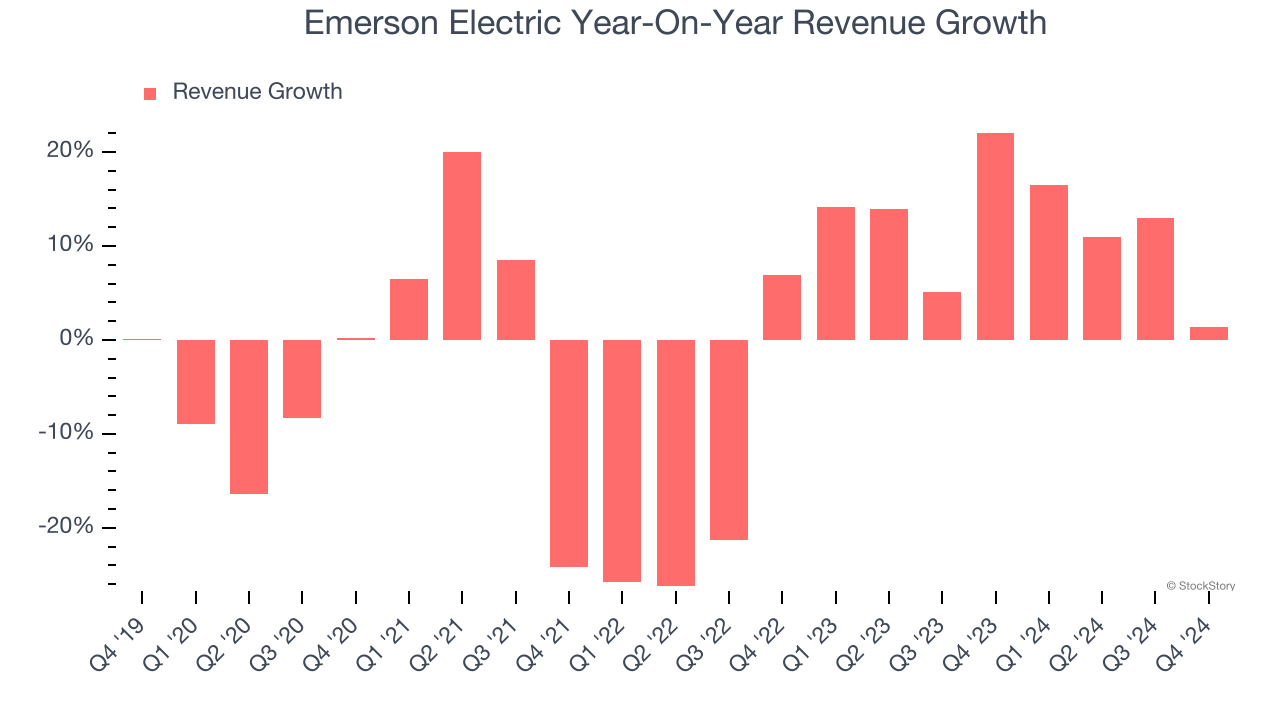

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Emerson Electric struggled to consistently increase demand as its $17.55 billion of sales for the trailing 12 months was close to its revenue five years ago. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Emerson Electric’s annualized revenue growth of 11.9% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Emerson Electric’s revenue grew by 1.4% year on year to $4.18 billion, falling short of Wall Street’s estimates. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

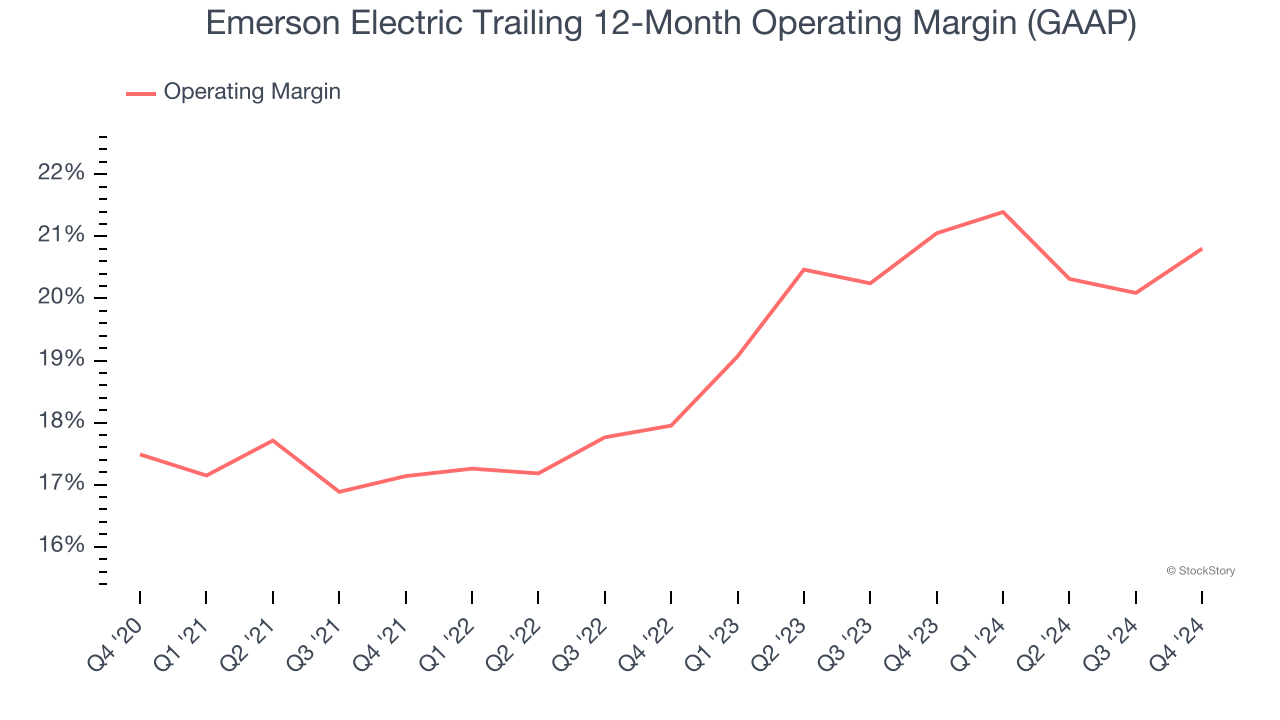

Operating Margin

Emerson Electric has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 18.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Emerson Electric’s operating margin rose by 3.3 percentage points over the last five years, showing its efficiency has improved.

In Q4, Emerson Electric generated an operating profit margin of 24.2%, up 3 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

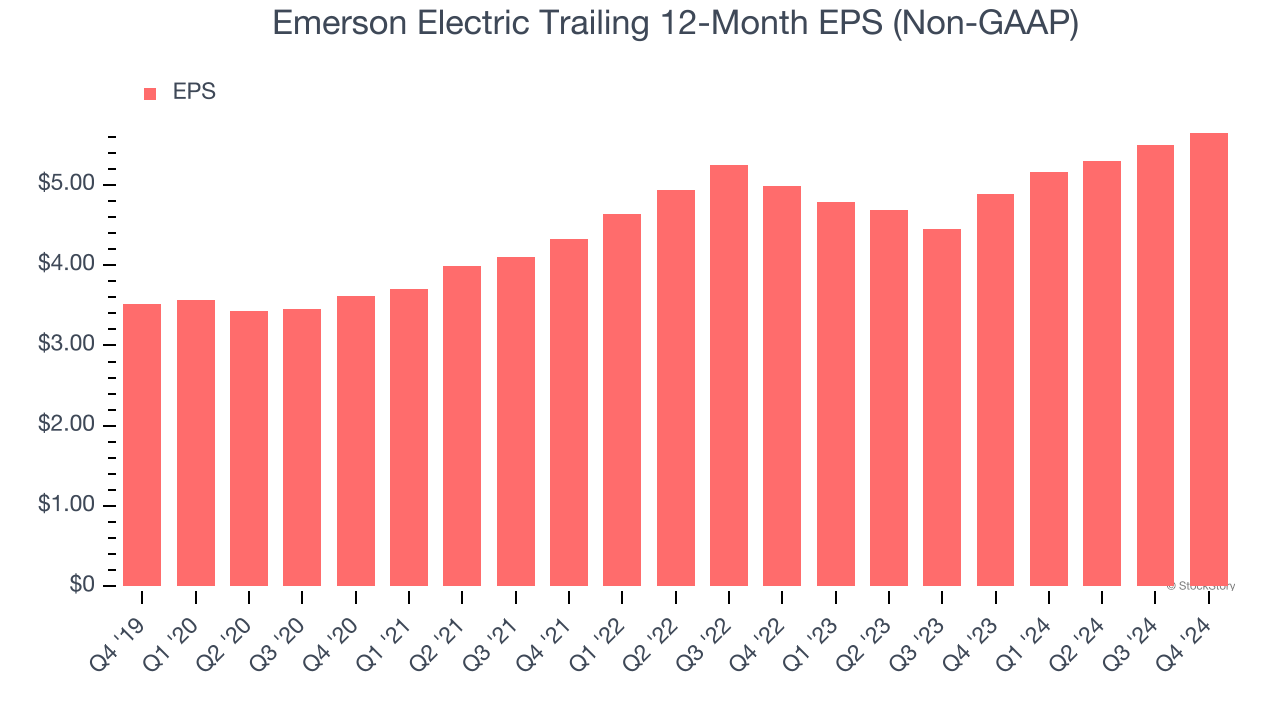

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Emerson Electric’s EPS grew at a solid 9.9% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

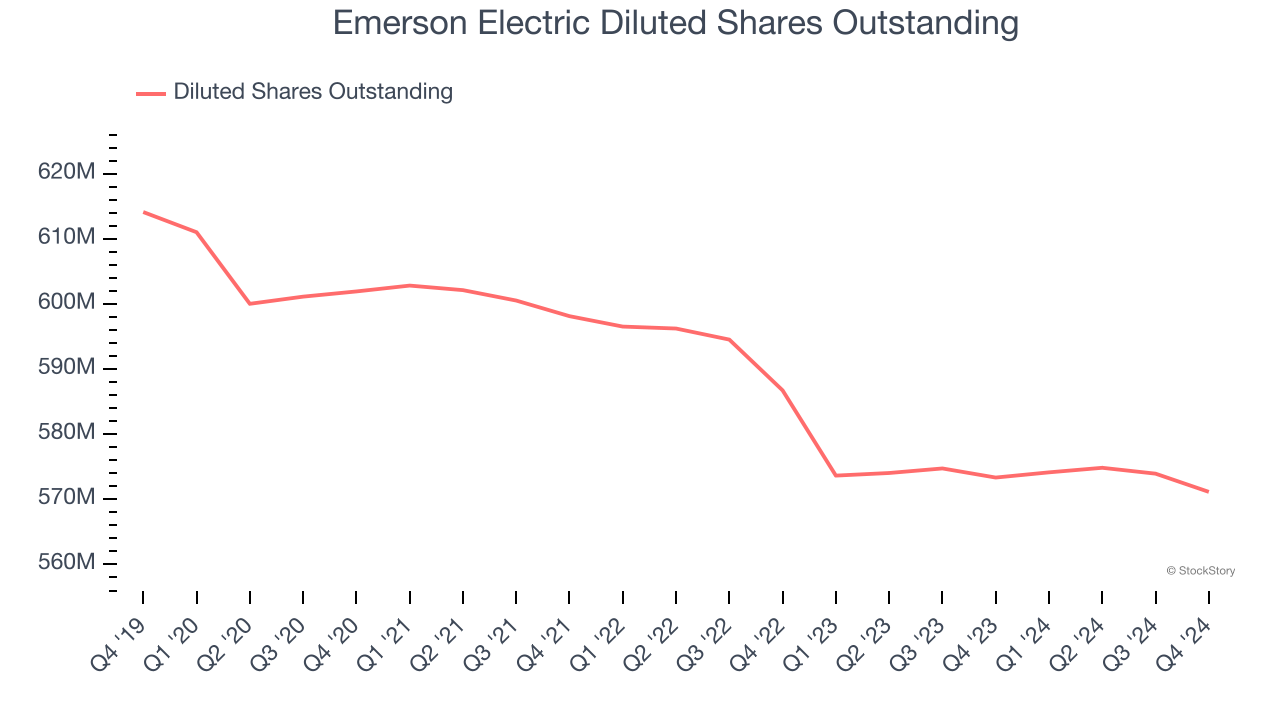

We can take a deeper look into Emerson Electric’s earnings to better understand the drivers of its performance. As we mentioned earlier, Emerson Electric’s operating margin expanded by 3.3 percentage points over the last five years. On top of that, its share count shrank by 7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Emerson Electric, its two-year annual EPS growth of 6.5% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Emerson Electric reported EPS at $1.38, up from $1.22 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects Emerson Electric’s full-year EPS of $5.65 to grow 7%.

Key Takeaways from Emerson Electric’s Q4 Results

We enjoyed seeing Emerson Electric exceed analysts’ EBITDA expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.1% to $125.05 immediately after reporting.

Big picture, is Emerson Electric a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.