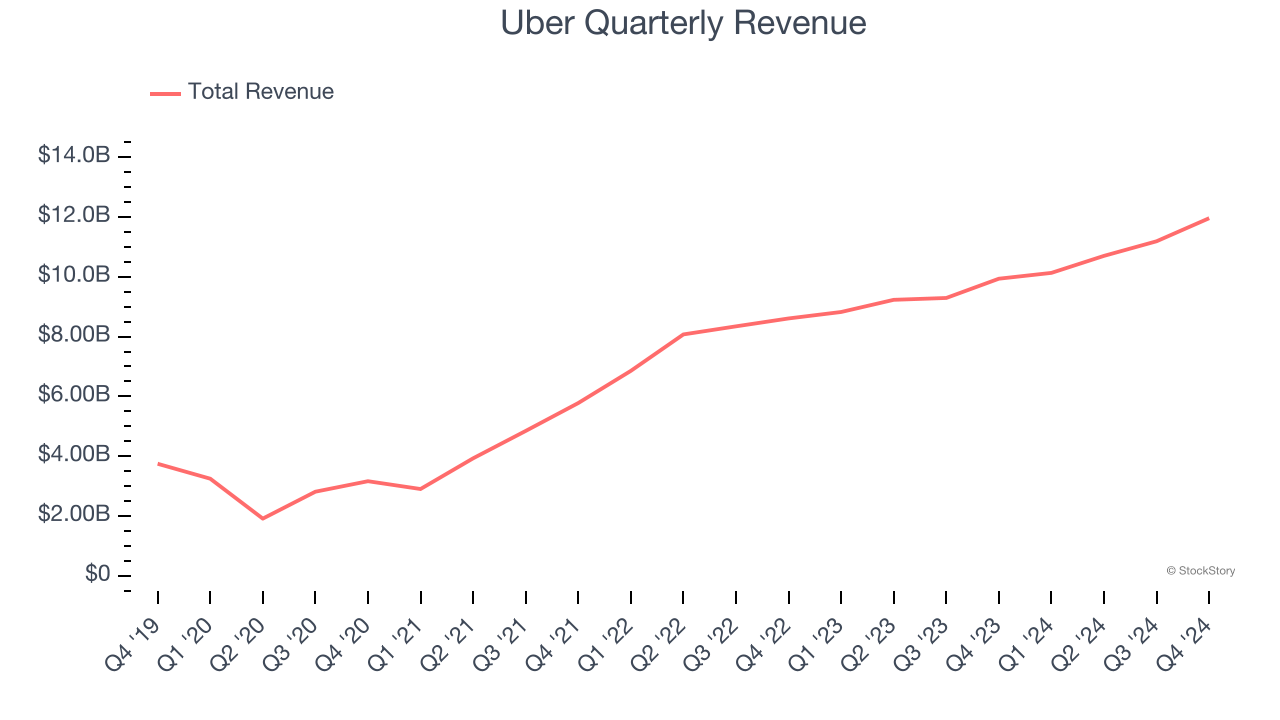

Ride sharing and on demand delivery service Uber (NYSE: UBER) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 20.4% year on year to $11.96 billion. Its GAAP profit of $3.21 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Uber? Find out by accessing our full research report, it’s free.

Uber (UBER) Q4 CY2024 Highlights:

- Revenue: $11.96 billion vs analyst estimates of $11.76 billion (20.4% year-on-year growth, 1.7% beat)

- EPS (GAAP): $3.21 vs analyst estimates of $0.48 (significant beat)

- Adjusted EBITDA: $1.84 billion vs analyst estimates of $1.85 billion (15.4% margin, in line)

- Q1 20215 Guidance: Gross Bookings of $42.75 billion at the midpoint (miss vs. expectations of $43.3 billion)

- Operating Margin: 6.4%, in line with the same quarter last year

- Free Cash Flow Margin: 14.3%, down from 18.9% in the previous quarter

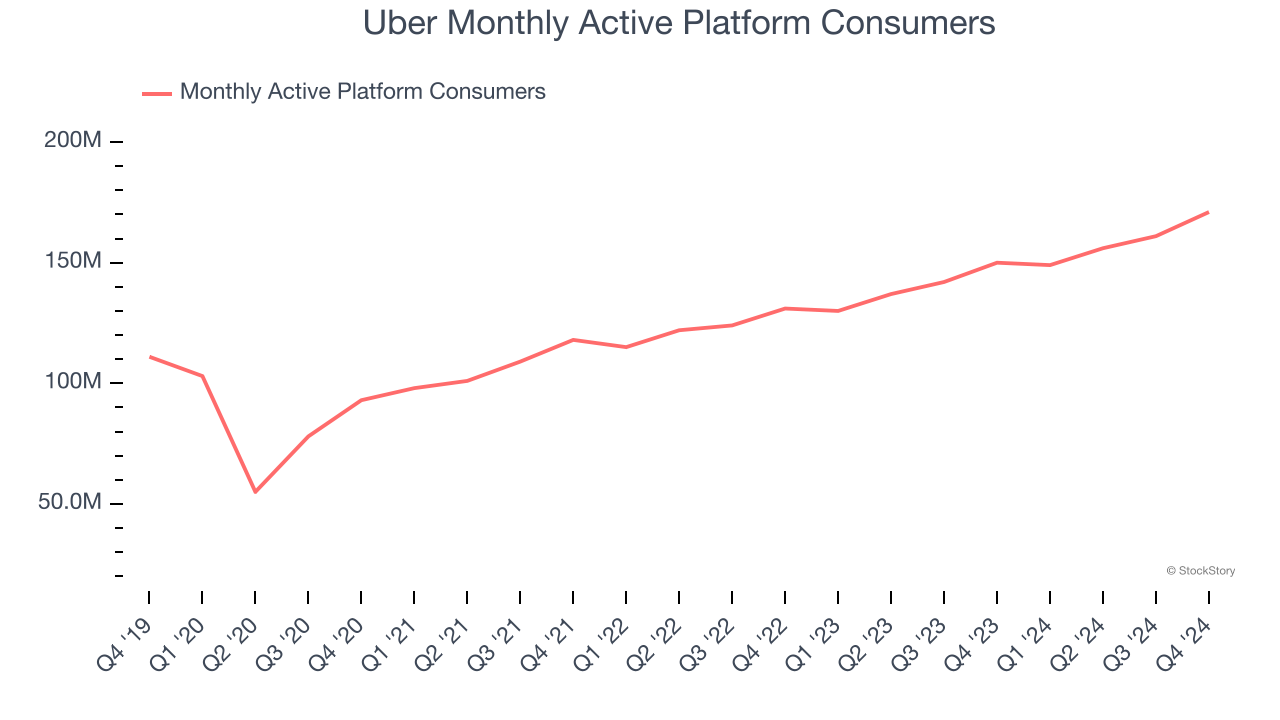

- Monthly Active Platform Consumers: 171 million, up 21 million year on year (beat vs. expectations of ~168 million)

- Market Capitalization: $146.9 billion

“Uber ended 2024 with our strongest quarter ever, as growth accelerated across MAPCs, trips, and Gross Bookings,” said Dara Khosrowshahi, CEO.

Company Overview

Born out of a winter night thought: "What if you could request a ride from your phone?" Uber (NYSE: UBER) operates a global network of on demand services, most prominently ride hailing and food delivery, and freight.

Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Thankfully, Uber’s 36.1% annualized revenue growth over the last three years was incredible. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Uber reported robust year-on-year revenue growth of 20.4%, and its $11.96 billion of revenue topped Wall Street estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 15% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and implies the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Monthly Active Platform Consumers

User Growth

As a gig economy marketplace, Uber generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Uber’s monthly active platform consumers, a key performance metric for the company, increased by 13.8% annually to 171 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q4, Uber added 21 million monthly active platform consumers, leading to 14% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

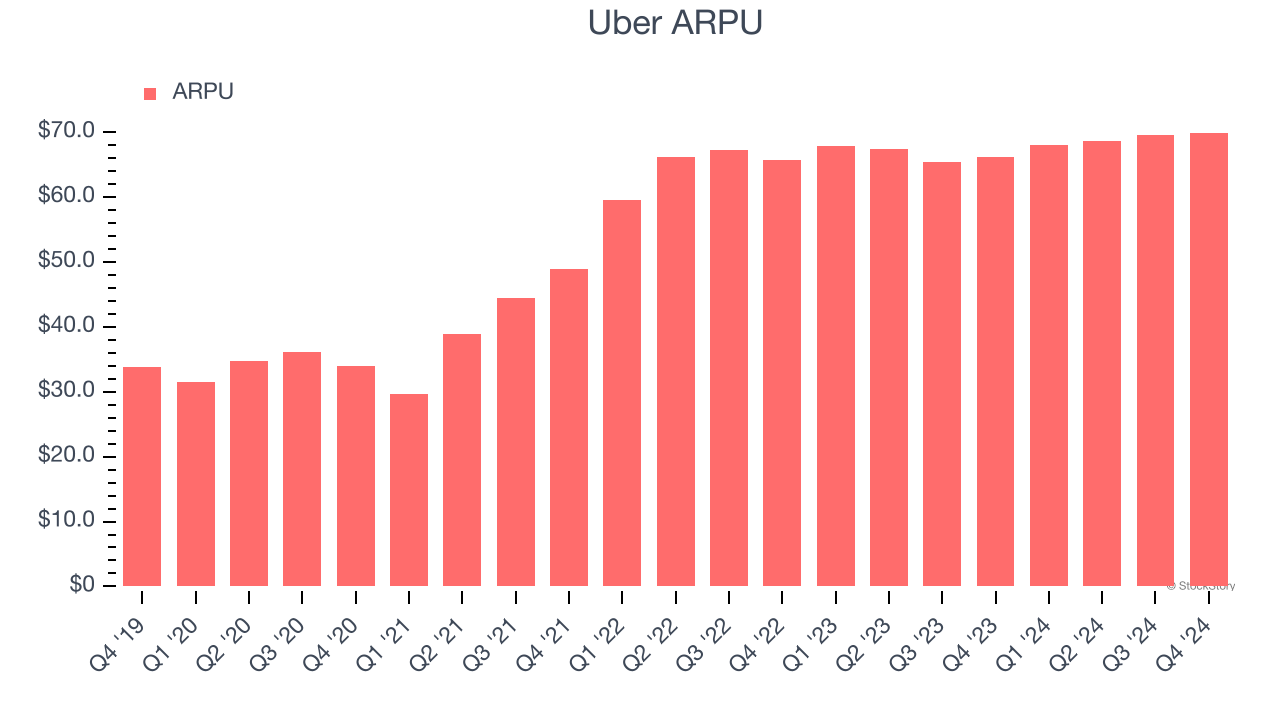

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for gig economy businesses like Uber because it measures how much the company earns in transaction fees from each user. This number also informs us about Uber’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Uber’s ARPU growth has been mediocre over the last two years, averaging 3.4%. This isn’t great, but the increase in monthly active platform consumers is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Uber tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Uber’s ARPU clocked in at $69.94. It grew by 5.6% year on year, slower than its user growth.

Key Takeaways from Uber’s Q4 Results

It was great to see Uber increase its number of users this quarter, beating expectations. This led to revenue outperformance. On the other hand, gross booking guidance for next quarter missed, and this is weighing on shares. The stock traded down 4% to $66.95 immediately following the results.

Is Uber an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.