What a fantastic six months it’s been for agilon health. Shares of the company have skyrocketed 65.7%, hitting $5.50. This run-up might have investors contemplating their next move.

Is it too late to buy AGL? Find out in our full research report, it’s free.

Why Does agilon health Spark Debate?

Transforming how doctors care for seniors by shifting financial incentives from volume to outcomes, agilon health (NYSE:AGL) provides a platform that helps primary care physicians transition to value-based care models for Medicare patients through long-term partnerships and global capitation arrangements.

Two Things to Like:

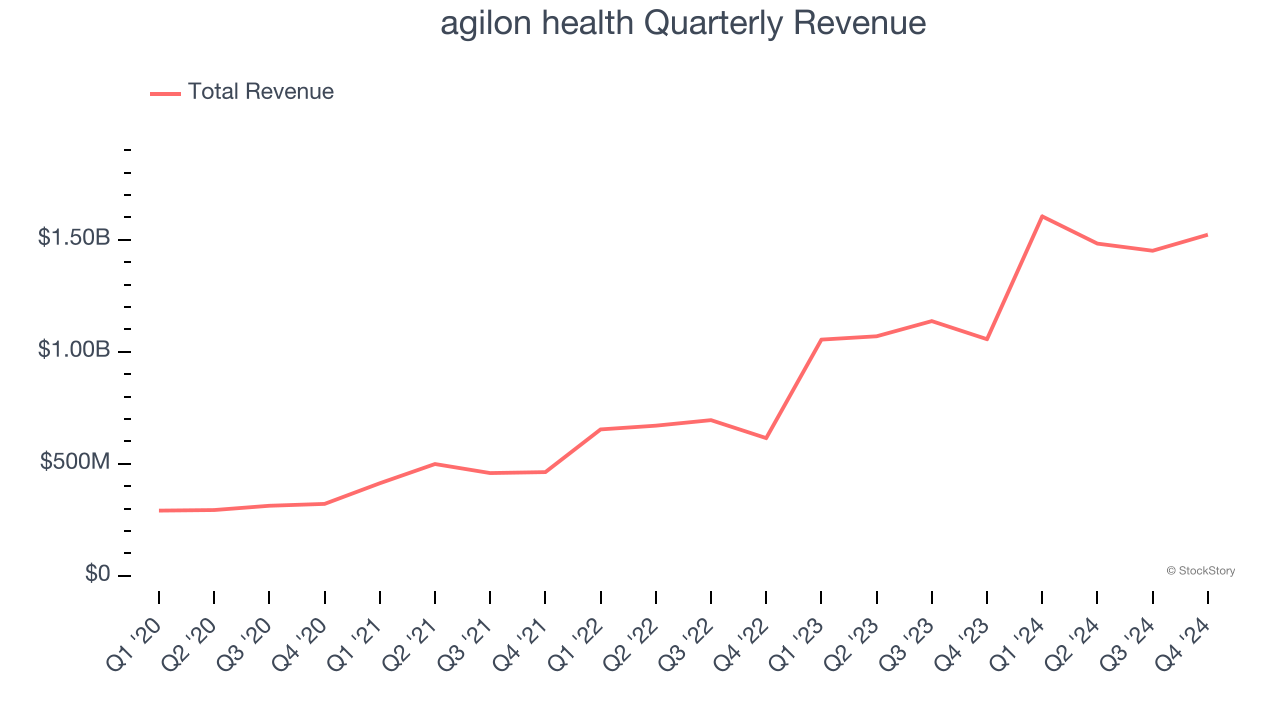

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, agilon health’s sales grew at an incredible 49.3% compounded annual growth rate over the last four years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

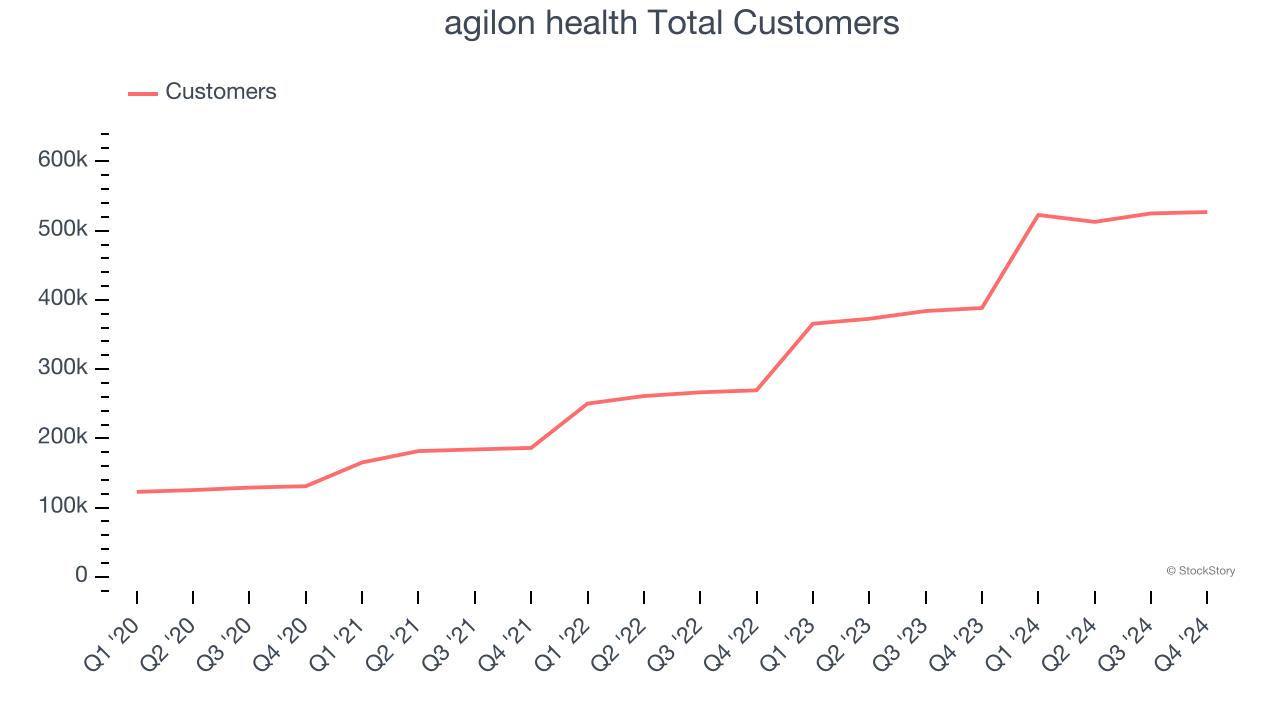

2. Customer Base Skyrockets, Fueling Growth Opportunities

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

agilon health’s total customers punched in at 527,000 in the latest quarter, and over the last two years, their count averaged 41.2% year-on-year growth. This performance was fantastic, reflecting its ability to "land" new contracts and potentially "expand" them later - a powerful one-two punch for sales.

One Reason to be Careful:

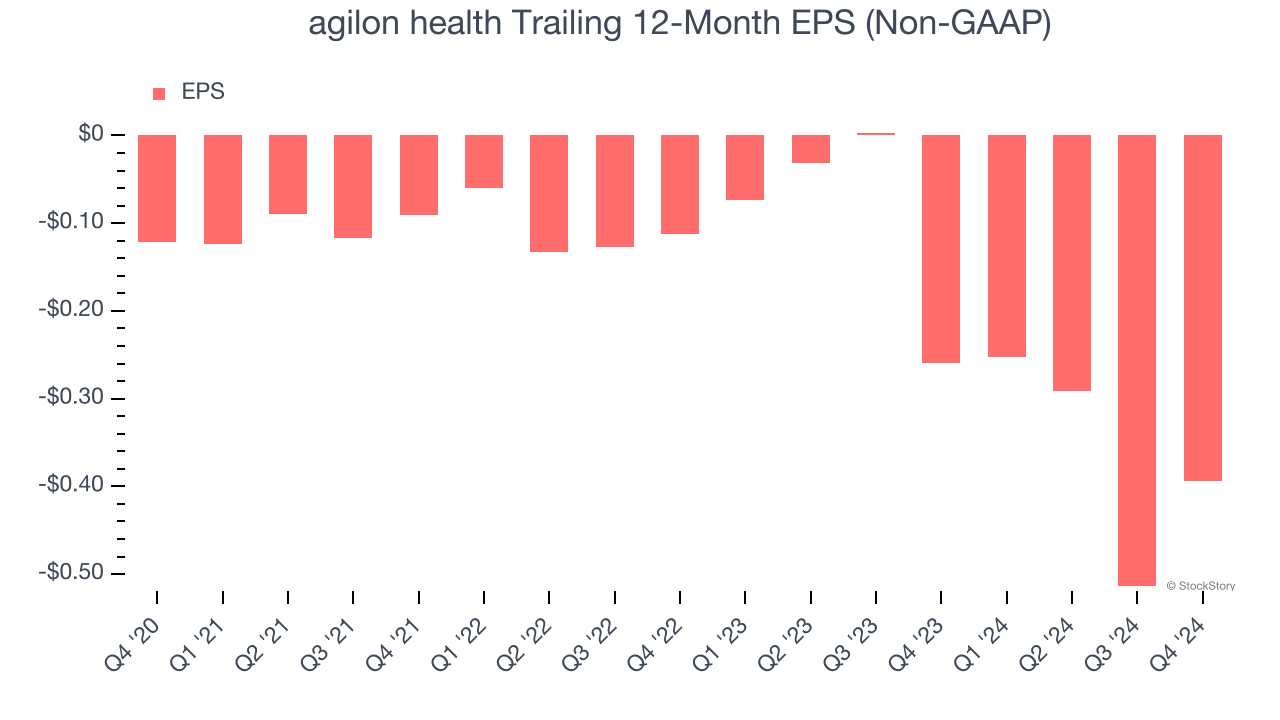

EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

agilon health’s earnings losses deepened over the last four years as its EPS dropped 34.1% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Final Judgment

agilon health’s positive characteristics outweigh the negatives, and after the recent rally, the stock trades at $5.50 per share (or 0.4× forward price-to-sales). Is now the time to buy despite the apparent froth? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than agilon health

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.