Over the last six months, Gap shares have sunk to $17.77, producing a disappointing 16.4% loss - worse than the S&P 500’s 6.9% drop. This might have investors contemplating their next move.

Is now the time to buy Gap, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the more favorable entry price, we're cautious about Gap. Here are three reasons why we avoid GAP and a stock we'd rather own.

Why Do We Think Gap Will Underperform?

Operating under the Gap, Old Navy, Banana Republic, and Athleta brands, Gap (NYSE:GAP) is an apparel and accessories retailer selling casual clothing to men, women, and children.

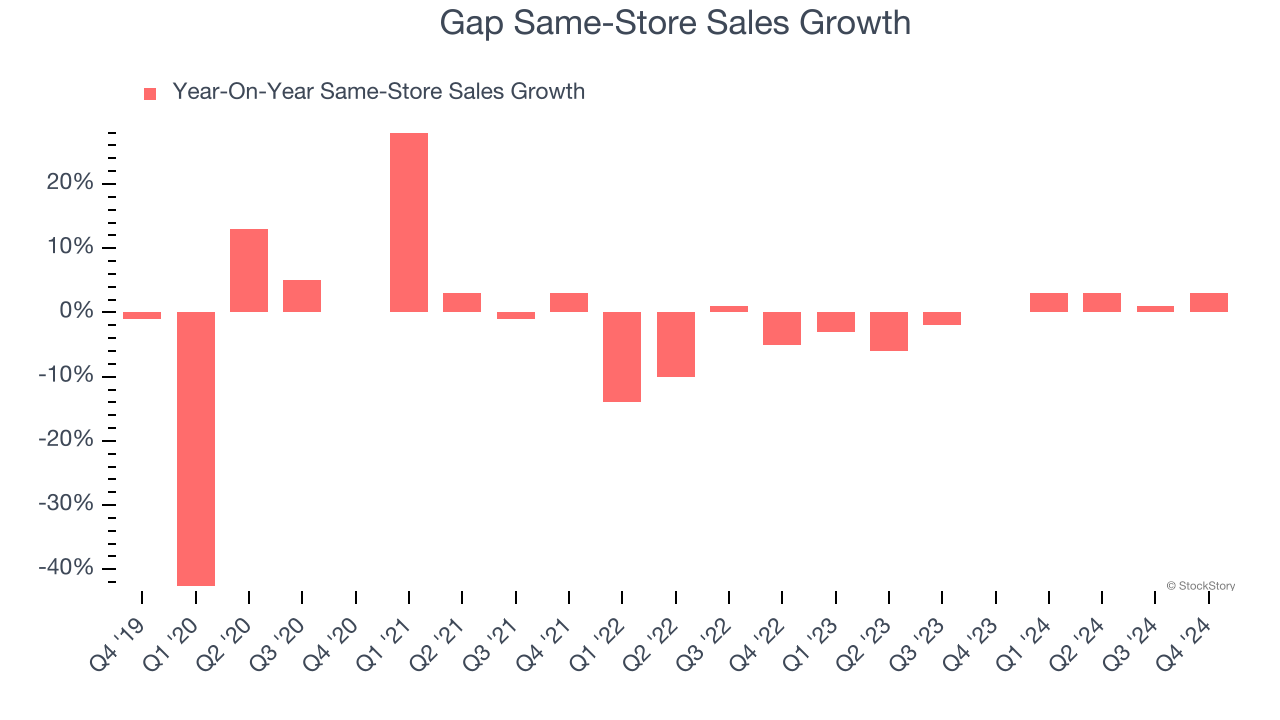

1. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Gap’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

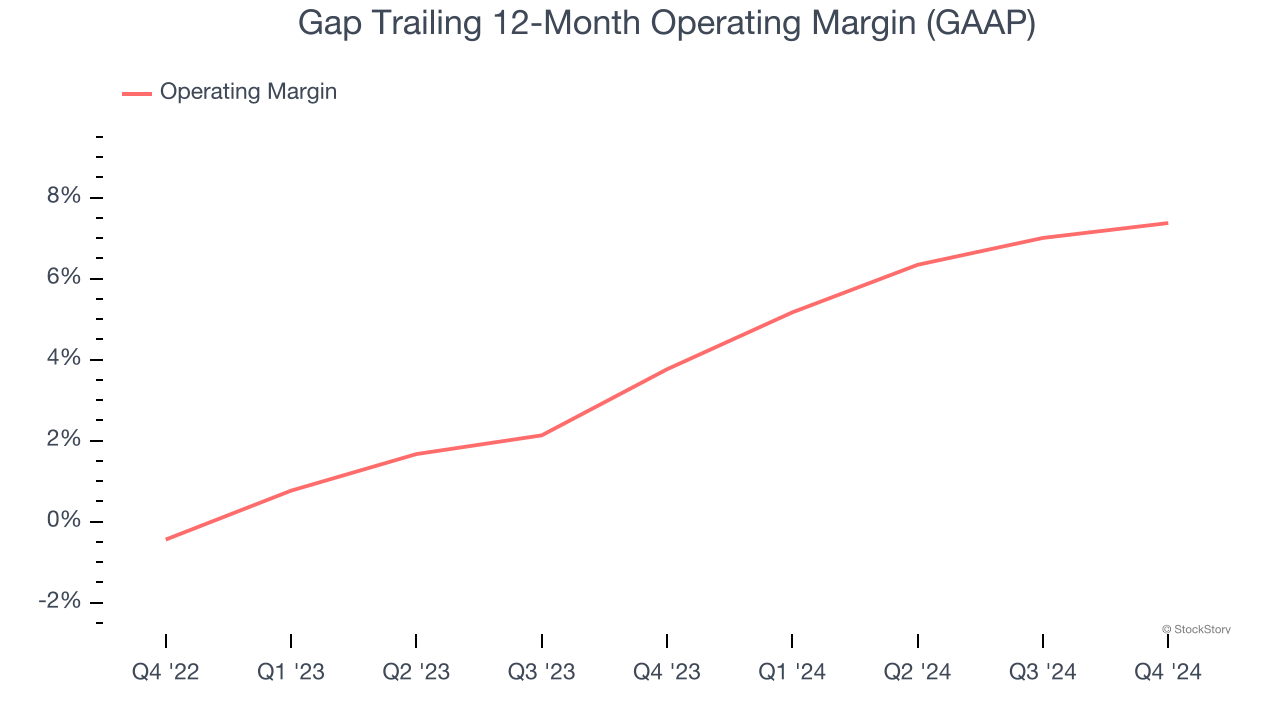

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Gap was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.6% was weak for a consumer retail business. This result is surprising given its high gross margin as a starting point.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Gap historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.3%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

Final Judgment

Gap falls short of our quality standards. After the recent drawdown, the stock trades at 8.2× forward price-to-earnings (or $17.77 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of Gap

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.